The Bau Project is Besra’s flagship gold asset, with which it has been associated since 2010. The Bau Project contains JORC 2012 compliant Resources exceeding over 3 Moz (on a 100% basis). In addition, it has a JORC 2012 defined Exploration Target as shown on the tables below. In January 2014 Besra released the Stage 1 Feasibility Study:

The Bau Project is Besra’s flagship gold asset, with which it has been associated since 2010. The Bau Project contains JORC 2012 compliant Resources exceeding over 3 Moz (on a 100% basis). In addition, it has a JORC 2012 defined Exploration Target as shown on the tables below. In January 2014 Besra released the Stage 1 Feasibility Study:

>> BAU PROJECT STAGE 1 FEASIBILITY STUDY (PDF download – 826 pages/48.6 MB)

Although limited in scope to an effective standalone development at the Jugan Hill deposit that study has provided critical guidance for planning the future strategy for optimising development of Bau, which following listing will entail:

- Resource Delineation

- Metallurgical Studies

- Processing Studies

- Upgrading Feasibility Studies

- Regulatory Compliance Management.

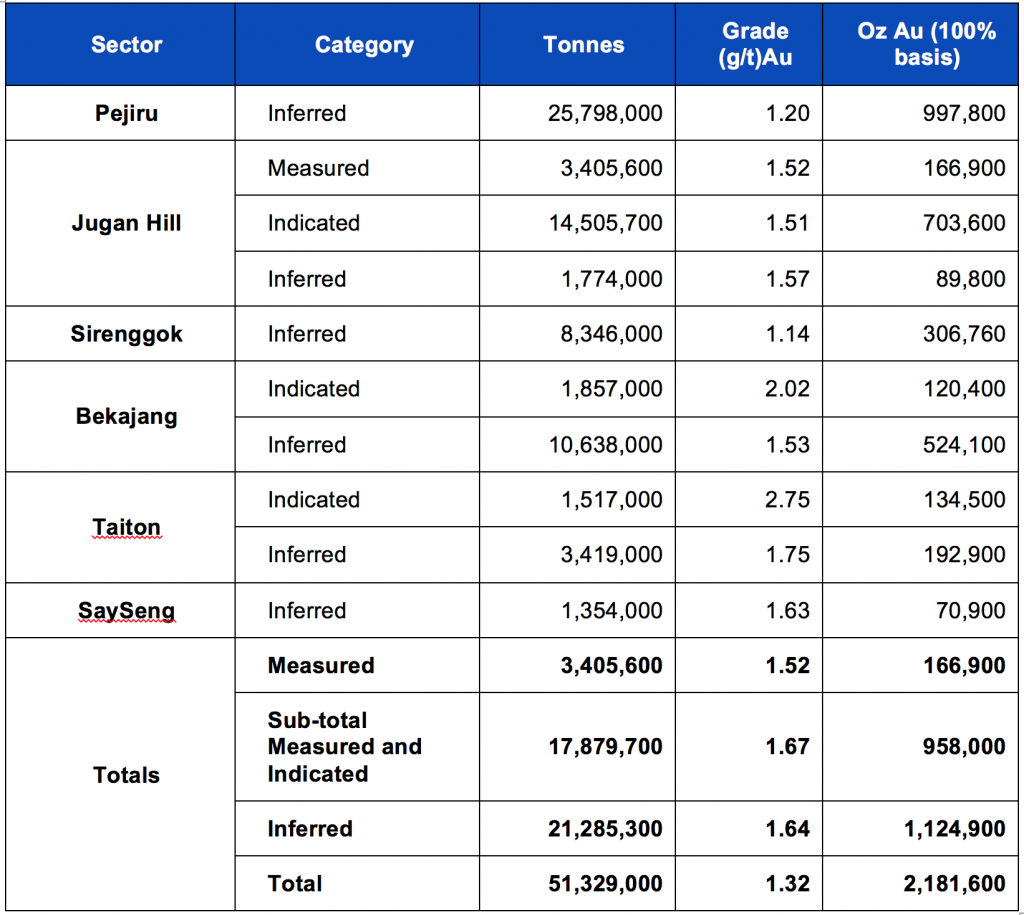

JORC Compliant Mineral Resources – Bau Gold Project (100% basis)

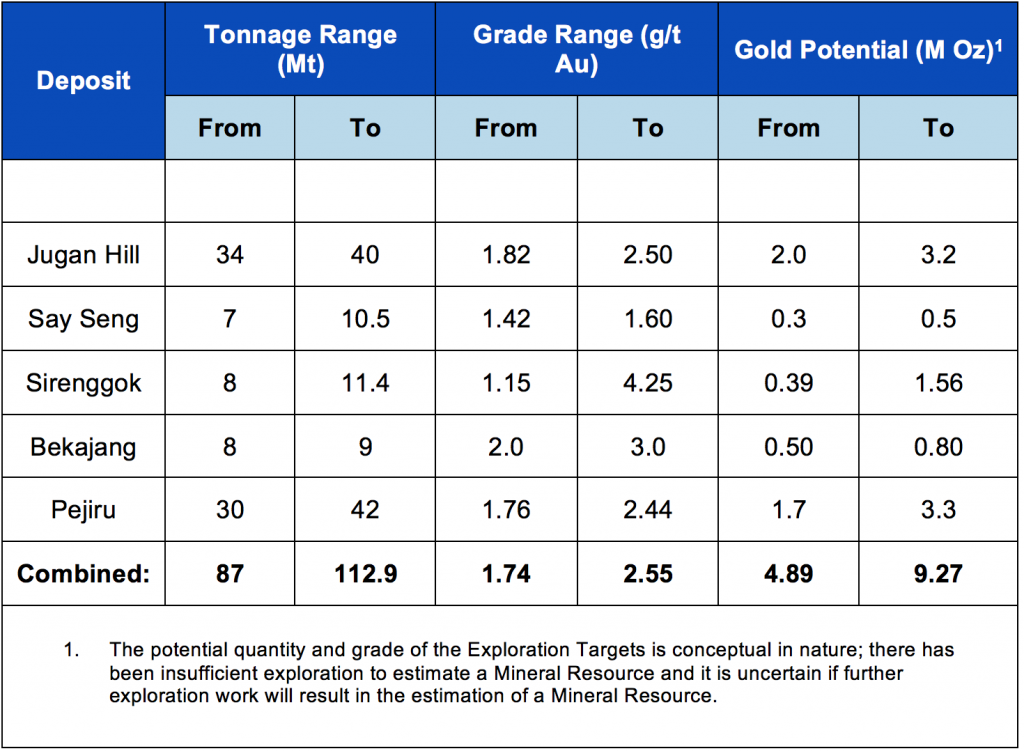

Exploration Target (100%) Basis – Bau

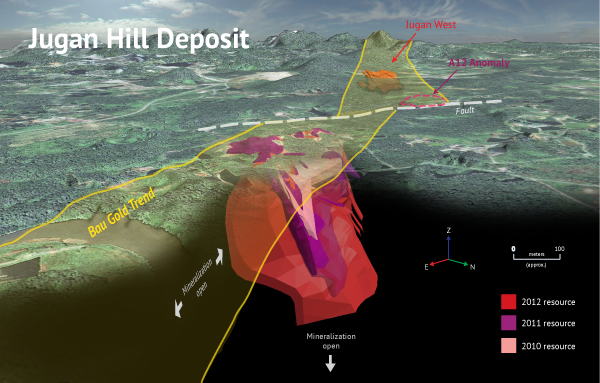

Southwesterly perspective of the Bau Gold Trend, showing Jugan Hill Deposit in foreground